Smart Ways To Use A Credit Card

Credit Cards can be a dividing issue when it comes to personal finance. However, when used responsibly, there can be a number of benefits to their use.

With this in mind, I’ve partnered with HSBC to explore smart Ways To Use A Credit Card. (Ad)

How can a credit card be beneficial?

If you have no existing debts, and are able to pay off the balance within the interest free period (either each month or within the offer time), then there can be several advantages to using a credit card.

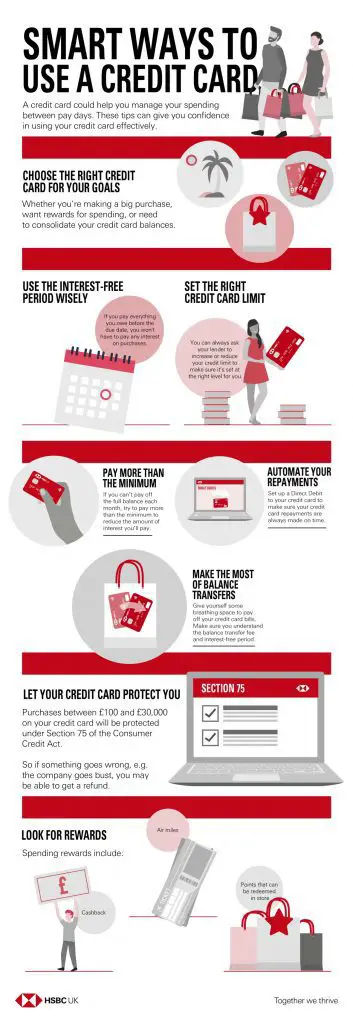

The biggest of these is consumer protection, and is the main reason I keep a zero balance credit card open today. Purchases between £100 and £30,000 made on a credit card are protected under Section 75 of the Consumer Credit Act, which means that large purchases such as a holiday are protected should a company go out of business. Typically, I would save for a holiday, purchase using the credit card, then pay off the balance straight away.

Building your credit rating is another benefit to using a credit card responsibly. If you are planning on applying for a mortgage, or taking out a personal loan, having a good credit rating can save you thousands on the interest rates you are likely to be offered.

With many credit cards you can also earn spending bonuses such as Air Miles, Cashback and reward points. This can be a useful bonus when using credit responsibly.

Use the interest free period wisely

You should always aim to pay off the balance of your card within the interest free period. Most standard cards give you a month to pay before any interest is calculated, but special 0% balance transfers and introductory offers can extend this period.

Set the right credit card limit

Make sure the credit limit is an amount you feel comfortable with, and easy to manage. If you are offered a credit increase you don’t feel comfortable with, you can request for this to be lowered.

Pay more than the minimum

I would always advocate paying off the balance in full within the interest free period, but when this isn’t possible, then paying more than the minimum is crucial. It can make such a difference to the repayment period – and amount of interest.

Automate Your Repayments

Never miss a payment again by setting up a monthly direct debit to your credit card. Even if you don’t know the amount you will need to pay each month, set a minimum amount to cover the minimum payment or more, and make an additional payment to cover the rest manually. Late or missed payments can seriously affect your credit rating, as well as the risk of fines or losing promotional rates.

If you currently have a credit card balance that is costing you interest, investigate if you can transfer to a better rate.

*Disclaimer: I would never encourage the use of a credit card while you are struggling to pay off debts. This post does not constitute professional financial advice.

Other Posts You May Like

Can You Save Money With HSBC Select and Cover?

Current Accounts Vs Savings Accounts – Understanding the Difference